Introduction: Operational Management of Boeing Company

Operations management deals with the ways organizations produce goods and services. Using transformation processes, it converts input resources, including information, material, and customers, by harnessing staff knowledge and facilities to meet external and internal customers’ needs. As such, though often not appreciated, it is present in every department of every organization.

Operations management exists at three highly interdependent levels that inform each other. The first is the corporate strategic level, where senior managers decide the long-medium term purposes and objectives for the organization as a whole. Additionally, the second level is operational, where middle-level managers dissect corporate strategy into specific departmental or functional purposes and medium to short-term objectives. Moreover, the third level is the supervisory management level, where operational objectives are dissected into a vast number of tasks and activities that have short term day-to-day time horizons. They usually have complex interdependencies across multiple tasks, departments, and external organizations. Individual managers are usually responsible for a great number of tasks that are simultaneously in play.

Importantly, within the second and third levels, the vast majority of an organization’s resources, particularly its people, exist, hence the sources of its short and long term capabilities. It is where competitive advantage and best practice performances can be achieved, provided the organization is continuously adapting to the threats and opportunities of its external environment and continuously implementing improvements (Schwalbe, 2008). Hence, operations management is a core element of organizational activity that focuses on the operational objectives of speed, quality, flexibility, and cost.

Nonetheless, it is important to acknowledge that processes are usually the fundamental baseline for the operations of all organizations. Therefore, it is important for all stakeholders to understand processes improvement, which is a core prerequisite of operations management in the organization. However, to be able to have effective and efficient process management, it is important to identify the key roles involved. According to Bryson (2011), these include the process worker, the process manager, the process owner, and the process sponsor.

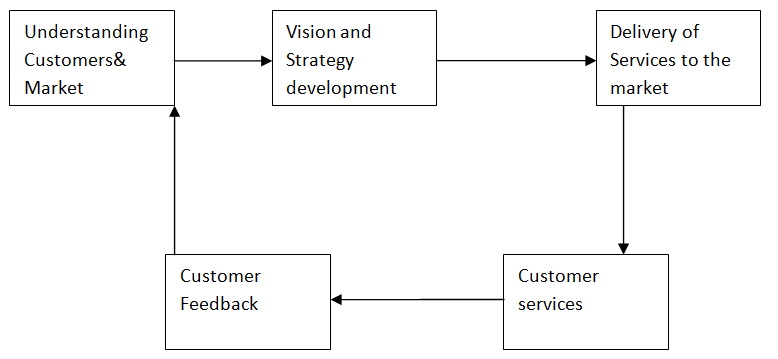

A balanced scorecard is, therefore, an approach that is used by most organizations in matters relating to operational management in order to meet the International Standards Organization (ISO) standards. Boeing Company should then continuously use the learning and growth perspective of the balanced scorecards to focus on its operational and management effectiveness, which is a recipe for continuous improvement of any organization. However, in implementing these balanced scorecards, the company needs to focus on customer service, finances, and the aspects of its internal operations (Ansoff, 1990). Nevertheless, Benshoff and Sean (2004) continue to affirm that in achieving these aspects, the company should utilize learning, innovation, and growth dimension as their basis of implementing the balanced scorecards in order to gain increased growth in its revenue turnover and to improve their service delivery through customer services.

As mentioned, operational management determines the management effectiveness of any organization. Therefore, the operational process for the Boeing Company will follow balanced scored cards. Boeing Company should then identify three major areas that are critical in the application of balanced scored cards in order to realize the desired results. These key areas for operational management include internal operations, financial management, and customer service (Berman and Evans, 2006). In respect to these, in order to successfully implement balanced scored cards in the company, it is imperative to examine each area of concentration by having measures in place to evaluate their learning and growth.

Customer Service

Any organization is in existence to serve a specific clientele. Service and product satisfaction of these clients guarantee the successful business operation of the entity. However, in order to have an outstanding customer service, the company’s management should acknowledge the need to have a learning and growth perspective that effectively address customer service through a variety of issues. For instance, company management should appreciate the need to hire people who are aligned with company values. Again, the company should realize the need of retaining those staff that provides outstanding customer service in its business operations. In doing so, quality, responsiveness, and speed in its customer service should be some of the measures that should be used to determine if this operational management is being implemented. Moreover, the company should ensure that it gets feedback concerning its customer service that relates to its operations. For instance, constant surveys should be conducted to evaluate customer satisfaction. Corrective measures should then be designed based on the customers’ feedback obtained.

Financial Management

Financial management is another key area of concern that balanced scored cards can be applied to bring forth operational management for the effectiveness of the company (Lynch, 2006). This can be achieved through a variety of ways. For instance, devising ways and means of improving costing information on customers is one of the ways that the company can implement its balanced scored cards in this area. In addition, the company should use monthly reports through meetings to communicate the financial state of the company. This is whereby customer based profitability should be compared to drive the company behavior (Borkowski, 2009). These monthly meetings should be used as a measure to determine the attainment of the learning and growth perspective in financial issues.

Nevertheless, according to Jenkins and Ambrosini (2002), financial assessment should be regularly conducted by the company to understand the true state of the company in terms of income in relation to its operating costs. Moreover, high volume clients should be targeted since they are the best recipe for improved financial performance. Nonetheless, company sales should also be monitored in order to optimize sales from the company’s goods and services. In addition, sales monitoring should be used as a learning and growth parameter in the implementation of balanced scored cards in financial issues.

Internal Operations

Balanced scored cards measures that should be applied in the internal operations of Boeing Company should also seek to address four crucial aspects. These aspects include; identification of new opportunities in the company processes and products, the deliverance of flawless products to its clients, to continually reduce costs, and to deliver what they say and when they say. However, for this to be achieved, several metrics have to be put in place. These metrics include clients’ satisfaction, which can be established through the evaluation of their feedbacks in relation to products and services (Johnson & Scholes, 2008).

Ways of improving the effectiveness and efficiency of the Balanced Scorecards

There exist causal chains effect of the objectives and measures of improving operational management. This is so since one objective leads to the potential achievement of another. The discussed categories (internal business, customer and financial perspectives) are intertwined to ensure achievement of the core mission, vision and objectives of the Boeing Company.

To begin with, to realize all these objectives in a more successful way, their implementation need to start with the learning and growth perspective where by measures such as continued training of employees need to be undertaken. In addition, under learning and growth perspective, employees of the organization should be constantly assessed to determine their performance in terms of service delivery in their daily operations.

With successful implementation of the learning and growth perspective, the process will then lead to internal business perspective. This is made possible as a result of a number of successful referrals and cross sells of the internal processes in the organization. A revolutionized learning and growth perspectives through proper training and assessment will guarantees improved internal processes of the organization.

Moreover, customer perspective follows internal business perspective. Under customer perspective, there are a variety of measures that needs to be used as metrics in ensuring implementation of this balanced scorecards. One major parameter that relates to this perspective is to determine the retention rate of the staff. For instance, it will be imperative that customer retention rate should be analyzed and examined to determine the percentage of the previous years that are still served by the organization. In addition, customer satisfaction ratings should be undertaken on the regular basis. After a successful implementation of the customer perspective, the implementation phase should then focus on financial perspective.

Financial Perspective

In respect to financial perspective, it should be implemented after customer perspective has already being administered. This is so since improved financial performance is only realized when customers in the business process of the organization meets customer needs. However, to ensure that the perspective is implemented successfully, several metrics need to be put in place. With respect to this perspective, the organization must assess financial aspects such as improved loans, deposits and the non interest income of the organization.

Implementation of the balanced scorecards in all branches of the Boeing Company needs to indicate positive impacts in all areas that are involved. For instance, the financial performance in all the branches of the company should be analyzed to determine whether implementation of the balanced scorecard process is helpful to the company. Any increase in financial performance will be a clear way to indicate that there is a positive financial growth in the previous fiscal years.

Moreover, the Boeing Company strategic goals need to be achieved through implementation of the balanced scorecard in conjunction to its strategic plans. Notably, improvement of the financial performance of the organization is one of the major company’s goals which other pillars of the organization are geared towards its realization. Since Boeing Company is not a charitable organization, it should be concerned more with the profit realization in its business operation. It is therefore imperative to note that all BSC approaches should be geared towards realizing a better performing organization in terms of its profit turnover.

However in respect to the attainment of the major strategic goals, the company should employ a variety of objectives that are geared towards supporting these goals. For instance, in respect to financial perspective of the balanced scorecard, the origination should have two objectives that seek to help realize these goals (Roberts, 1984). Increase in profit turnover is tantamount to improvement of financial performance. Thus, increase in profit indicates that the company is doing well to financial related matters. In addition, all efforts that can be put in place to increase profit in the organization are recipes to improved financial performance.

In addition, increase in revenue is another objective that should help to achieve strategic goals. Increase in revenue is a clear indication that the organizational business operation are performing well. Therefore, this has a direct relationship to improved financial performance since revenue will only increase when there is improved business operations (Lock, 2007). Therefore, it is a common knowledge that matters that relates to financial aspects in the company will have contributory impacts to the status of the organizational financial performance hence a determinant of company’s operational process performance.

Collaboration, Cooperation and Coordination in Implementing Balanced Scorecards for Boeing Company

Operational process implementation of the balanced scorecards just like its formulation must follow defined approach to achieve the desired result. Nonetheless, it is important to have collaboration, cooperation and coordination in the implementation process. According to Bryson (2011), implementation of strategies acts as a transition from their planning phase where they are incorporated in different sub systems of the company to bring the desired value.

With respect to the Boeing Company, collaboration, cooperation and coordination are crucial in the effort of achieving the desired outcomes as intended in the company’s strategic plans. Therefore, there is need for the management and the entire stakeholders of the company to practice these values in order to realize effectiveness and efficiency as it is desired in its strategic plan. Nevertheless, it is postulated by Koteen (1997) that collaboration, cooperation and coordination in the implementation process of any organization have several roles that help to attain targets in the strategic plan.

To begin with, according to Clegg and Hardy (1999), collaboration, cooperation and coordination in the implementation process of strategy plan have a role of creating and sustaining a coalition that supports implementation of changes. However, for the coalition to be created there is need for all stakeholders of the Boeing Company to have good working relationships that are characterized by collaboration and cooperation and where people are willing to share ideas while working in harmony. This ensures realization of the common good for the organization. Nonetheless, it is also relevant that the implementation process should be overseen by good coordination exercise so that tasks can be synchronized to avoid conflicts that that may occur as a result of poor organization (Ehnert, 2009).

Moreover, Healey (1997) opined that it is important to acknowledge collaboration, cooperation and coordination in implementation process of the strategy plans. This helps to prevent likelihood of failure that may come as a result of resistance. Consequently, this usually occurs as a result of negative beliefs and attitude towards desired changes that strategic plans may desire to achieve (Landskroner, 2002). However, in respect to Boeing Company, the company should seek to carry out education of its stakeholders concerning strategic plans in effort of reducing resistance to changes in the implementation process.

Furthermore, it is relatively important to note that collaboration, cooperation and coordination in the implementation phase help to create a network that may help to redesign an environment in the company that can ensure long term changes (Jackall, 1988). This is important since these elements can help stakeholders in the organization to act as one team. As a result, any change in management like transfer of senior management from the company will still render it viable since it is build on pillars of collaboration, cooperation and coordination.

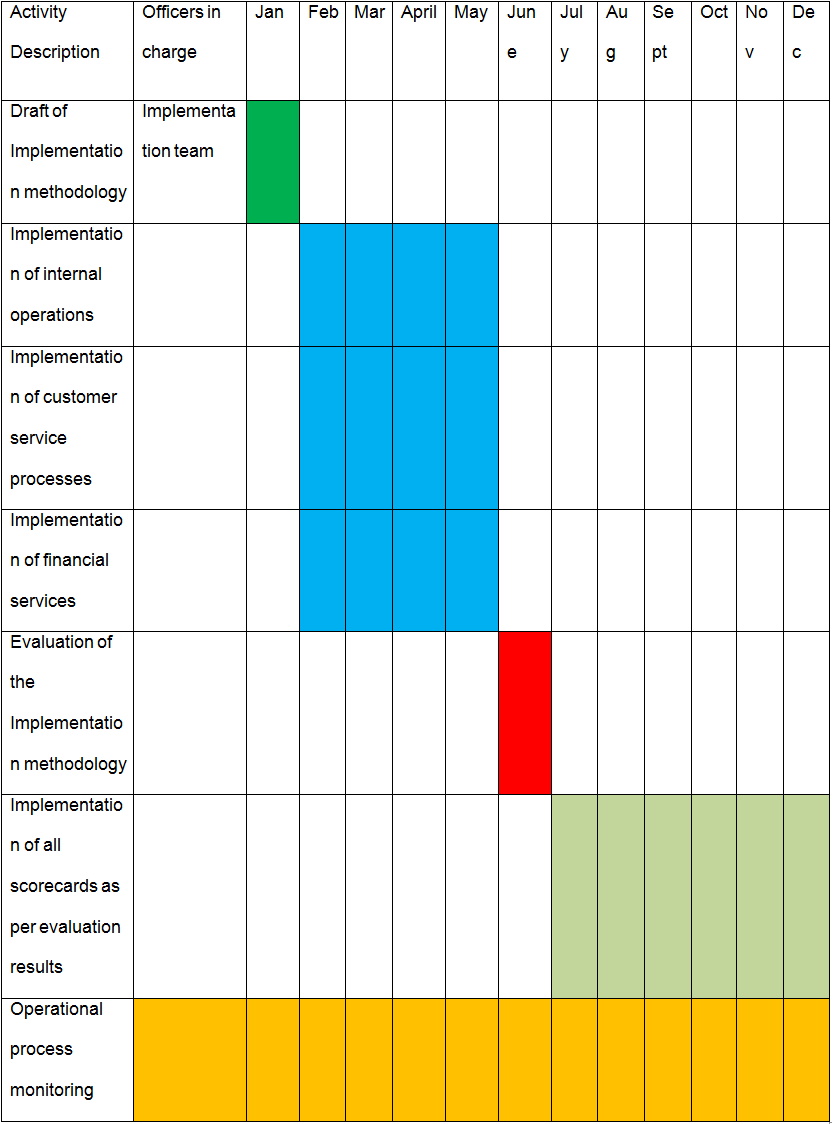

Balanced Scorecard Operational Process Implementation Gantt chart

Budget

The total cost of the implementation phase of the operational process of the balanced scorecards has been split into parts to indicate the exact cost estimates that every activity in the entire management is expected to cost.

Total project cost: $203, 000.00

Draft of implementation methodology: $35,000.00

Implementation of internal operations: $28,000.00

Implementation of customer service processes: $95,000.00

Implementation of financial services: $ 12,500.00

Evaluation of the Implementation methodology: $14,000.00

Implementation of all scorecards as per evaluation results: 15,500.00

Operational process monitoring: $3, 000.00

Assessment of risks involved and proposal of their containment

Importantly, Knights and Roberts (1982) believed that it is relative to acknowledge that every project has risks that always pose threats to the project success. Therefore, for this project, a number of risks come into fore as potential threats for the success of the entire project. The risks include:

- Poor communication amongst team players

- Change resistance by some stakeholders

- A threat of not meeting clients needs

- Financial constraints

- Poor Return on Investment

- Unforeseen risk for example, natural Disaster

In respect to all these risks, there is need to have good risk management plan in place that is desired to tackle each and every risk identified. For instance, in terms of poor communication amongst team players, there is need to develop good team work culture which can be achieved through teamwork building efforts such as having retreats (Heerkens, 2007). Moreover, change resistance is also likely to be addressed through proper communication strategies. For instance, all plans that are intended to be implemented in the operational process should be communicated to all stakeholders to win their support.

Moreover, threats that touch on failures to meet users’ needs and requirements should also be closely monitored through constant review to ensure that the resultant product address users’ needs. However, it is important to acknowledge that user needs keeps on changing from time to time (Haynes, 2002). For that matter, it is important that developers of the company’s products and services should constantly review users’ needs to ensure that the final product is in conformity with the needs of users at the time of delivery.

However, it is relatively important to have a risk management team in place to ensure that that operational implementation process is well guarded against these risks (Lynch, 2006). For instance, there should be a consultant who is well versed with the process of continuous improvement to provide expert advice during implementation phase.

Nonetheless, in respect to financial constraints, it is imperative that the company’s management should be in support of the operational process in order to provide necessary resources for its implementation. However, there should be an implementation team with a team leader in order to monitor the implementation process to guarantee its return on investment (Roberts, 1984). Lastly, the risk relating to natural disasters can be contained through having a proactive and reactive disaster management programme in place.

To wind up, the operational process management of Boeing Company can apply balanced scorecards that involved three major operational areas that are integrated together to ensure that the management is successful. However, for the operational process to be successful it is important that right from its initiation to planning, to execution, there must be proper monitoring and controlling which must run throughout the operation of the company. Moreover, constant evaluation of the programme must be constantly undertaken to take desired corrective measures.

References

Ansoff, H. (1990) Implementing Strategic Management. London, Prentice Hall.

Benshoff, H. & Sean, G. (2004) America on film. UK, Blackwell Publishing.

Berman, B. & Evans, J. (2006) Retail Management, A Strategic Approach. London, Prentice Hall. 5.

Borkowski, N. (2009). Organizational Behavior, Theory, and Design in Health Care. Canada, Jones & Bartlett Publishers.

Bryson, J.M. (2011) Strategic Planning: For Public and Nonprofit Organizations. U.S, John Wiley & Sons, Inc.

Clegg, S.R. & Hardy, C. (1999) Studying Organization: Theory and Method. London, Sage.

Ehnert, I. (2009) Sustainable Human Resource Management. London, Springer.

Haynes, M.E. (2002) Project management: Practical tools for success. 3rd ed. New Delhi, PHI Learning Ltd.

Healey, P. (1997) Making Strategic Spatial Plans: Innovation in Europe. London, Routledge.

Heerkens, G.R. (2007) Project management: 24 steps to help you master any project. US, McGraw Hill.

Jackall, R. (1988) Moral Mazes: The World of Corporate Managers. Oxford, Oxford University Press.

Jenkins, N. & Ambrosini, V. (2002) Strategic Management: A Multi-Perspective Approach. Basingstoke, Palgrave.

Johnson, G. & Scholes, K. (2008) Exploring Corporate Strategy. 8th Ed. London, Prentice Hall.

Knights, D. & Roberts, J. (1982) The power of organization or the organization of power? Organization Studies, 3(1), pp. 47-63.

Koteen, J. (1997) Strategic Management in Public and Nonprofit Organizations. US, Greenwood Publishing Group, Inc.

Landskroner, R.A. (2002) The Nonprofit Manager’s Resource Directory. New York, John Wiley & Sons, Inc.

Lock, D. (2007) Project Management. 9th ed. England, Gower Publishing Ltd.

Lynch, R. (2006) Corporate Strategy. 4th Ed. London, Prentice Hall.

Roberts, J. (1984) The moral character of management practice. Journal of Management Studies, 21(3), pp.287-302.

Schwalbe, K. (2008) Introduction to project management. 2nd ed. US, Cengage Learning.