Introduction

Chapter twelve highlights the importance of inventory management in different business organizations. Inventory management is a crucial tool that is essential in the management of inventory, which is the most expensive asset of many companies. Good inventory management help organizations to reduce costs and operations managers should recognize the critical role played by inventory in their organization (Heizer and Render, p. 468).

Summary of chapter twelve

Chapter twelve highlights the functions of inventory to organizations. Four functions are discussed in this chapter. Firstly, inventories provide a hedge against inflation and upward changes in raw material prices. Furthermore, inventories enable organizations to quantity discounts that are associated with purchases made in large quantities, hence reducing the cost of goods on their delivery. Inventory is also crucial in decoupling demand fluctuations. This enables the firm to provide a stock of goods from which customers can choose (Heizer and Render, p. 469). Finally, inventory enables firms to separate various parts of the production process (Heizer and Render, p. 468).

Four types of inventories are maintained by firms. The raw material inventory contains raw materials that have been purchased by a firm but have not been processed. This inventory eliminates variability in quality, quantity, or delivery brought about by suppliers of raw material. Work-in-process inventory is composed of raw materials that have entered the process.

Maintenance/repair/operating (MRO) inventory is critical in keeping machinery and processes on track. This inventory is pivotal in ensuring the timely maintenance and repair of processing equipment. The last inventory is known as finished-goods inventory, which contains finished products that are ready for sale and shipment to customers or to meet future customer demands (Heizer and Render, p. 468).

For effective inventory management, the operations manager should carefully control critical items through the classification of the items into different classes to assign costs per unit. Additionally, firms should keep accurate records of all inventories as well as properly account for classified items to eliminate any inaccuracies in the records of inventories kept. These three control ingredients help the firm to avoid inventory shrinkage and pilferage (Heizer and Render, p. 471-473).

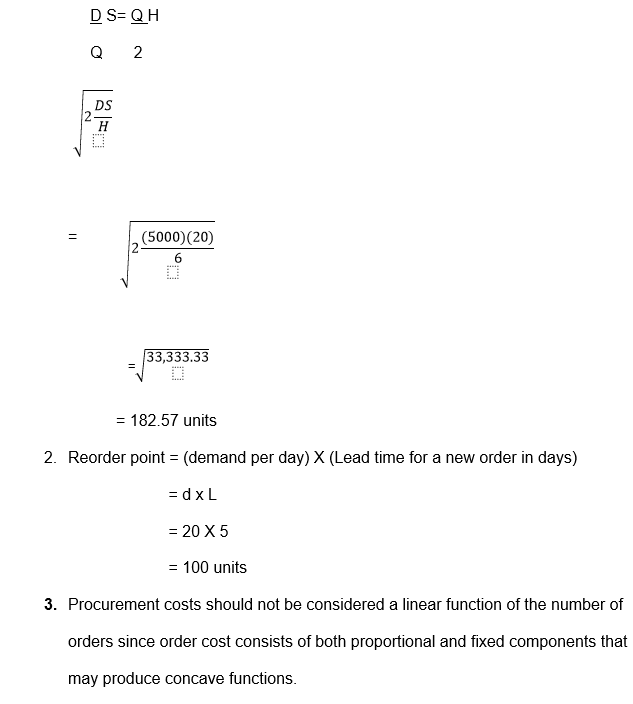

Inventory models are essential in the control of holding, ordering, setup, and setup time costs. There are several independent inventory models that try to give solutions to the questions of where to order and how to order inventory. These inventories include Basic Economic Order Quantity (BOQ), Production Order Quantity Model, and Quantity Discount Model (Heizer and Render, p. 474). The three models assume that the demand for goods is constant and certain. On the other hand, probabilistic models are real models meaning that the demand for a product is variable and uncertain.

The above models are a fixed-quantity ordering system that orders the same amount of inventory each time. However, the perpetual inventory system takes note of the changes in records. Therefore, perpetual inventory systems keep current records of inventories. Fixed-period inventory is a system in which inventory orders are made over a given period. A fixed-period inventory system ensures that inventories that are required to bring inventory to target levels are ordered (Heizer and Render, p. 493).

Question

Optimal order quantity is found when annual setup (order) cost equals annual holding cost (p. 477).

Works Cited

Heizer, Jay H. and B. Render. Principles of Operations Management. Upper Saddle River, New Jersey: Pearson Prentice Hall, 2006. Print.