Introduction

Management plays a significant role in the success and running businesses. Therefore, selecting the best approach to management is critical. It is worth noting that businesses operate in dynamic environments. As such, business leaders should incorporate the changes in the environment in the running of businesses to enhance success and sustainability (Huynh, Gong, & Huynh, 2013; Pan, Baird, & Blair, 2014).

For instance, recent developments have forced organizations to pay attention to processes, activities costs, and performance measurements. Moreover, it is now vital to emphasize key elements such as customer satisfaction, reliability, cycle time, flexibility, and productivity, which are critical for customer satisfaction, value addition, and businesses’ goal attainment (Ismail, 2010; Kumar & Mahto, 2013).

Moreover, the success of a business is based on continuous involvement of the management of all activities to guarantee high-quality service putting in mind the need for the highest levels of efficacy. As such, adopting the conventional accounting principles may be ineffective and, therefore, approaches that provide information on every activity are needed (Ismail, 2010; Bahnub & Cokins, 2010; Roztocki, 2010).

In the 1980s, an expert in management, Kaplan, came up with activity-based management (ABM) to address issues pertaining to the information on activities within organizations (Roztocki, 2010; Roztocki, 2010). ABM is a management technique where managers are tasked with ensuring continuous improvement in planning and operational control by giving considerable emphasis on operational activities (Ismail, 2010).

ABM is an approach to management in which process managers are given the responsibility and authority to improve the planning and control of operations by focusing on key operational activities. As such, managers and policymakers use accounting information to comprehend and improve the activities in organizations (Cardos & Pete, 2011; Roztocki, 2010).

Components of the ABM approach to management tend to resonate with key stakeholders in an organization since day-to-day activities are expressed in terms of occurrences/events that are familiar to all participants, including sale personnel, purchasing managers, inspectors, material handlers, and other employees (Huynh et al., 2013).

It is imperative to note that ABM purposefully integrates critical elements such as activity analysis, activity-based costing (ABC), activity-based budgeting, and value chain analysis, among others (Bahnub & Cokins, 2010; Kumar & Mahto, 2013; Cardos & Pete, 2011).

This research paper focuses on elucidating and explain the ABM concept as used in management. Key elements of the ABM are comprehensively discussed. Information is obtained from scholarly resources, including articles from peer-reviewed journals and management books.

Literature Review

Although the topic of activity-based management attracts the attention of many stakeholders, especially because it is considered an alternative a better alternative to the traditional cost management, pundits argue that there is no enough research material. There was an increase in the publication of articles since the development of the approach in the 1980s. However, a drop in publication was witnessed in the late 1990s (Cardos & Pete, 2011). Currently, many scholars publish articles on the implementation of ABM in specific industries or firms.

Ismail (2010) combined of a case study and survey approaches to investigate the application of ABM on an institution of higher learning. The author appreciated the fact that managing modern universities has been made more difficult by the dynamic environment where the digital revolution affects most elements of education. Therefore, there are needs to adopt ABM, which appropriate in controlling cost and improving and maintaining high-quality education. Therefore, managers of universities can adopt ABM for the purposes of determining costs of provision of products, reducing cost where appropriate, improving efficiency in goal attainment, and providing high-quality education to customers.

Roztocki (2010) used e-commerce to investigate the application of ABM in modern companies. The author suggested that the application of ABM in e-commerce is vital. E-commerce has developed, especially over the last few decades, and therefore, the traditional cost management requires improvement to deliver effectively. Therefore, e-commerce companies’ managers could adopt ABC/ABM managerial approach since it entails giving accurate activities costs for products, services, and projects. Moreover, e-commerce managers could use ABC/ABM to trace costs and allocate them to specific activities and, therefore, highlight and eliminate unnecessary cost, which negatively affects e-commerce profitability.

Pan et al. (2014) investigated the relationship between organizational life cycle (OLC) stages and the use/success of the ABM management approach among different companies. Their study revealed that firms at the maturity and revival stages used ABM more comprehensively in relation to organizations in the other stages of OLC. As such, it could be argued that managers of companies at the maturity stage consider the assigning of cost to activities and improving efficiency as crucial to the success of the business. Nevertheless, it is important to use ABM at every stage of OLC since the results indicated that the success of ABM practices is not influenced by stages.

Huynh et al. (2013) gave a discussion on how the concepts of ABB an ABM could be integrated to augment efficiency and add value to products. The authors described ABM as a popular approach to management due to its leveraging characteristics, especially when compared with the traditional cost management approaches. They noted that ABM could not address all the problems associated with modern cost management, especially supporting information for managerial decision-making processes. As such, it is imperative that modern firms go beyond tracking and assigning costs to activities by integrating ABM practices with pertinent and related techniques such as activity-based budgeting.

Discussion on the Overview of ABM

Features of ABM

Activity-based management is an integrated administration methodology, which captures an entire organization as a whole system and stresses the need to focus on activities with the main purpose of augmenting and improving customers’ value, which is considered a prerequisite for attaining profits (Huynh et al., 2013).

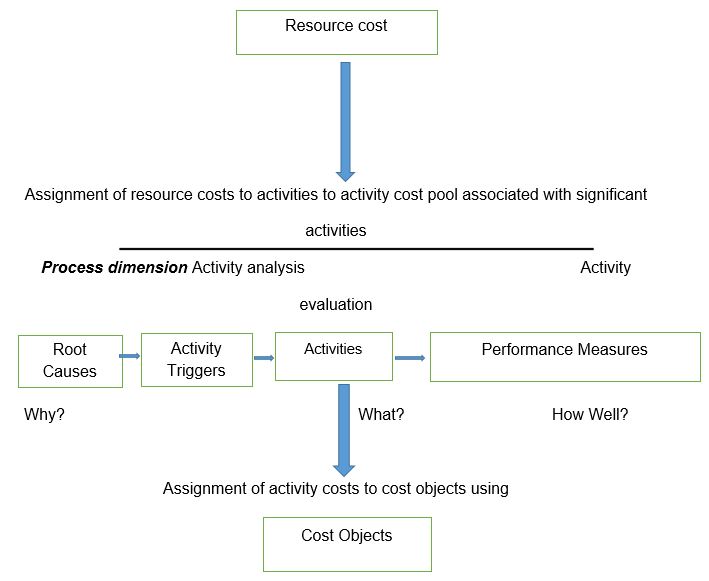

It is imperative to understand that ABM depends on activity-based costing (ABC) as the source of information. Therefore, ABM could be subdivided into two broad dimensions, including the cost aspect and the process element (Huynh et al., 2013). The cost aspect of ABM gives critical information on “resources, activities, and cost objects of interests such as products, customers, suppliers, and distribution channels” (Huynh et al., 2013, p. 182). The key purpose of the cost dimension of the ABM technique is to improve the accurateness of cost projects.

The cost of all resources in a firm is drawn from related activities, while all costs of undertakings are allocated to cost objects (Huynh et al., 2013). As such, the ABC aspect of ABM is beneficial for merchandise costing, strategic cost management, and strategic analysis (Huynh et al., 2013).

On the other hand, the process dimension of ABM is comprised of the providing of information concerning what activities are carried out in a firm, their rationale, and the efficiency/effectiveness in their performance (Huynh et al., 2013).

As such, the process dimension of the ABM technique is concerned with what, why, and how activities are carried out in the entire organizational system. Moreover, it is imperative to note that the process aspect of ABM is geared at reducing costs. Therefore, the main objective of the process dimension is ensuring effectiveness with the highest efficacy. Further, the process aspect of ABM allows managers, policy makers, and other pertinent stakeholders to participate and evaluate continuous improvement within firms/organization (Huynh et al., 2013).

Cost dimension

The above diagram is a representation of the two dimensions of ABM as discussed by (Huynh et al., 2013). While the cost dimension is represented by the section above the black line, the process dimension is denoted by the section below the line.

The Role of ABC in ABM

In many studies, the terms activity-based management (ABM) and activity-based costing are used together. In some instance, ABM and ABC are used interchangeably. However, it is worth noting that although the two aspects work together, they do not entirely mean the same thing. The output of one of the two elements of management is the input of the other. As such, ABC and ABM should function together for effectiveness and efficiency (Cardos & Pete, 2011; Kumar & Mahto, 2013; Roztocki, 2010).

Huynh et al. (2013) proposed that the principle of ABM is using the output of ABC system to enhance and inform decision-making processes and improve operational control. As such, ABM uses ABC in enhancing operational efficacy and goal attainment, especially augmenting value and profitability through identifying opportunities for improving strategy and operations within a firm.

Essentially, ABM entails the actions organizational managers take, based on ABC assessments and evaluations, with the aim of augmenting operational efficacy (activities efficiency) and increasing merchandise profitability (Huynh et al., 2013; Cardos & Pete, 2011; Kumar & Mahto, 2013).

Moreover, ABM uses ABC output to make improvements in processes, especially the processes that involve batch and product-sustaining activities within a firm.

According to Huynh et al. (2013), “ABC system is used to improve the operations of an organization in ABM” (p. 182). As such, firms that adopt the ABM management technique should also use ABC to augment processes. It is the nature of businesses and organizations to get involved in activities, which inevitably are associated with cost. As such, ABC plays a crucial role in measuring and tracking the cost associated with activities carried out in a firm over time. Moreover, the ABC system is vital in gathering information that is significant in ABM since the technique is based on gathering data on organizational financial /operational performance regarding important activities (Huynh et al., 2013).

Huynh et al. (2013) asserted that managers who use ABC and ABM together are motivated in two ways. To begin with, the technique allows the assigning of costs to activities. As such, it is easy to get information on which activity caused a certain cost. Moreover, since ABC/ABM technique allows assigning of cost to activities, it is easy to identify redundant costs and eliminate them. By eliminating unnecessary costs, ABM/ABC transforms loss-making products to profitable commodities and eliminates loss production operations (Huynh et al., 2013; Ismail, 2010; Kumar & Mahto, 2013).

In an endeavor to elucidate whether ABC and ABM should be used together or separately, Cardos and Pete (2011) asserted that ABC is critical for the ABM management approach. The authors proposed that ABC should be the basis of ABM since ABC entails the measuring of “the cost and performance of activities, resources, and cost objects” (p. 157). The assigning of activities to their respective costs and allocating each activity to cost object is the basis of ABC and ABM interaction.

Cardos and Pete (2011) depicted ABM as an approach to management that ABC data to focus on redirecting and enhancing effective usage of resources to augment values creation. As such, for ABM to focus on the management of activities, stakeholders should consider adopting ABC as a source of pertinent information.

It is worth noting that there are instances where ABC could become ABM. Cardos and Pete (2011) indicated that ABC could be considered ABM in cases where it is used in:

- Designing products and services that exceedingly satisfy customers while realizing considerable profitability

- Indicating instance where continuous or discontinuous enhancement in quality, efficacy, and speed are desired

- Informing decision-making process

- Selecting the best suppliers

- Negotiating pricing, product feature, quality, and customer value

- Adopting efficient distribution

Using the table below, Cardos and Pete (2011) demonstrated how ABC and ABM function together to accomplish objectives.

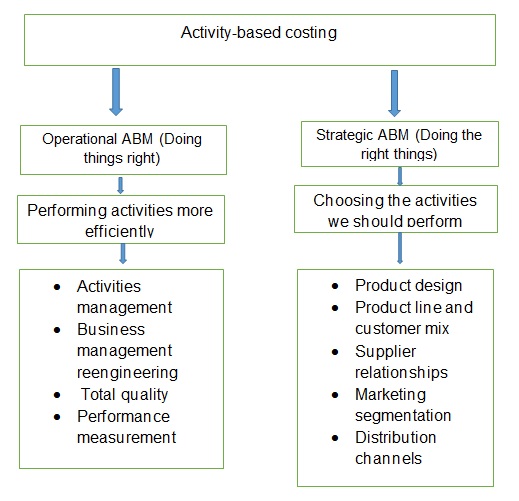

From the table above, it is apparent that (Cardos & Pete, 2011) implied that ABM could be categorized into two broad classifications, including operational ABM and strategic ABM.

Operational ABM

The authors described operational ABM as the technique that aims at enhancing operational efficacy, reduce cost, and promote optimal asset utilization. As such, operational ABM promotes the doing of things the right way (Cardos & Pete, 2011).

Operational ABM could be used to increase capacity through various techniques such as, reducing equipment/machinery downtime, reducing/eliminating errors/faults, and increasing operational efficiency. Firms that adopt operational ABM are highly likely to benefit in various ways, including reduced costs, high revenues resulting from optimal uses of resources, and avoidance of redundant costs (Cardos & Pete, 2011).

Strategic ABM

Cardos and Pete (2011) described strategic ABM as a management approach that searches for various techniques that an organization could adopt to create and sustain a competitive advantage and, therefore, promote doing the right things. In general, Cardos and Pete (2011) considered ABM as an approach that attempts to alter demand activities to upsurge profitability, making optimal product designs, and enhancing stakeholder relationship.

Purpose and Outcomes of ABM

As discussed earlier, ABM approach to management was developed to address issues of cost management, especially due to the failure of the traditional methods (Bahnub & Cokins, 2010; Ismail, 2010).

One of the outstanding element of ABM is assigning the cost to activities. The technique uses various attributes of data tags for every particular cost incurred in the carrying out of activities in firms. Data attributes make it possible for managers to perform analysis of various dimensions of management issues (Bahnub & Cokins, 2010; Kumar & Mahto, 2013; Cardos & Pete, 2011).

According to Cardos and Pete (2011), companies that implement ABM practices are likely to realize five elementary information outputs, including pertinent information regarding costs of activities/operations, the cost of non-value-added activities, activity-based performance methods, precise product/service cost, and cost drivers.

Moreover, ABM/ABC is a vital approach that informs decision-making processes on crucial matters such as product pricing, management, and upgrading of products in a firm. As such, the ABM/ABC practices provide comprehensive comprehension of cost and activities (Cardos & Pete, 2011; Kumar & Mahto, 2013).

Conclusion

This paper has used secondary resource material to explain the ABM approach to management. It is evident that ABM is a vital technique that has gained popularity among enterprises and organizations since its inception in the early 1980s.

Managers prefer ABM technique to the traditional methods due to its efficacy and clarity in dealing with management accounting, especially with recent developments in the global environment of doing business.

From the literature material used in the paper, it is apparent that ABM is a management approach that gives managers the responsibility and authority to ensure continuous improvement in planning and operational control by focusing on operational activities.

ABM approach to management resonates with many stakeholders in any firm because day-to-day activities are expressed in terms of occurrences/events that are familiar to all stakeholders.

Corporations that use all the ABM practices are probable to appreciate fundamental information outputs, comprising information regarding costs of activities/operations, the cost of non-value-added activities, activity-based performance approaches, exact product/service cost, and cost drivers. In addition, the ABM/ABC technique to management is vital in informing decision management processes.

ABM is oftentimes integrated with related concepts such as ABC and ABB. ABC is a technique that involves measuring of cost Vis a Vis operational activities. As such, resources are allocated to activities and activities to cost objects. Therefore, ABC is considered integral aspects of ABM where the earlier functions as inputs to the later.

ABM practices could be categorized into two broad groups, including operational ABM and strategic ABM. Operation ABM entails improving operational efficacy, cutting cost, and promoting optimal asset utilization. Essentially, operational ABM ensures that things are done in the right way within organizations. On the other hand, strategic ABM is a management approach that seeks opportunities to create and sustain leveraging aspects and, therefore, promote doing the right things.

Alternatively, ABM could be divided into two dimensions, which are cost aspect and process element. The cost dimension of ABM entails providing vital information on resources, activities, and cost objects, and is aimed at improving accurateness in costs projects. On the other hand, the process dimension of ABM comprises the provision of information regarding the activities carried out within and organization, their justification, and how effectively they are done. In addition, the process dimension of ABM is aimed at reducing cost and enhancing efficacy while allowing managers to carry out continuous improvement evaluations.

Although ABM is better in addressing cost management issues in relation to the traditional methods, the technique needs further development. Moreover, more research on the topic is required.

References

Bahnub, B. J., & Cokins, G. (2010). Activity-based management for financial institutions: Driving bottom-line results. Hoboken: New Jersey: John Wiley & Sons.

Cardos, I. R., & Pete, Ş. (2011). Activity-based costing (ABC) and Activity-based management (ABM). Journal of Economic Literature, 32(41), 151-168.

Huynh, T., Gong, G., & Huynh, H. (2013). Integration of activity-based budgeting and activity-based management. International Journal of Economics, Finance and Management Sciences, 1(4), 181-187. Web.

Ismail, N. A. (2010). Activity-based management system implementation in higher education institution: Benefits and challenges. Campus-Wide Information Systems, 27(1), 40-52. Web.

Kumar, N., & Mahto, D. (2013). Current trends of application of activity-based costing (ABC): A review. Global Journal of Management and Business Research Accounting and Auditing, 13(3), 1-15.

Pan, T. N., Baird, K., & Blair, B. (2014). The use and success of activity-based management practices at different organizational life cycle stages. International Journal of Production Research, 52(3), 787-803. Web.

Roztocki, N. (2010). Activity-based management for electronic commerce: A structured implementation procedure. Journal of Theoretical and Applied Electronic Commerce Research, 5(1).