Introduction

This paper examines the usefulness of the balanced scorecard in measuring the success of an organization. Performance measurement is a critical success factor for any organization, particularly in the competition-driven market. The concept of performance assessment refers to the process of gathering, analyzing, and reporting information on the extent to which an individual or organization is achieving the set objectives or profitability (Bititci, Garengo, Dörfler, & Nudurupati, 2012). The measurement may be meant for the entire organization or even a single process or strategy. The aim is to determine whether the output is by the organization’s goals. One of the most common performance measurement tools is the balanced scorecard (BSC). This management system allows organizations to perform several actions such as communicating goals, aligning the organization’s goals with the strategy, and/or monitoring progress. Areas of evaluation include the organization’s mission, vision, and core values. As the paper reveals, the BSC measures an organization’s processes by classifying them into four perspectives, namely, financial measures, customers, internal processes, and innovation/ improvement.

Background (Background and History of the Concept)

A BSC is a tool that was established to close the gap between the core elements of the organization (mission, vision, and strategy) and the operational elements of objectives, measures, key performance indicators (KPIs), and targets. BSCs have gained popularity in use across various sectors, including business, the government, and industries. Wu (2012) asserts that nearly half of all large organizations in the US use the BSC. Further, this measurement system is gaining popularity in Europe and Asia, owing to the growing need for organizations to outshine their rivals. Additionally, the BSC is easy to use because the semi-structured tool relies on design methods, which in turn help in tracking business activities by the management of an organization. The use of individual scorecards to manage performance is the commonest use of the tool. However, it is also useful in strategic management.

Kaplan and Norton (1993) were the first people to introduce the BSC as a strategic management system. In this capacity, the tool performs the following functions:

- Focusing on the strategic agenda of the company

- Identifying and monitoring data systems

- Selection of financial and non-financial data

Earlier performance measurement tools failed since they could not incorporate the strategy into the measurement of day-to-day processes. By the1993, the concept of the BSC had been smoothened by eliminating the minor flaws, which made it quite applicable for most businesses (Kaplan & Atkinson, 2015). At the time, it became clear that the developers needed to create a cause-and-effect approach regarding the four perspectives being measured by the BSC. This approach was now being referred to as “performance modeling”, as opposed to the earlier performance driver models. The cause-and-effect linkage made it possible to monitor functions/projects and their impact on the organization. Later, developers thought it wise that objectives should be highlighted before the measures.

Discussion

From the time of its invention to date, the BSC has continued to grow in prominence. Some of the largest organizations in the world use it, for instance, Google Inc. As explained earlier, it aligns the organizational chart with the day-to-day goals. As such, it can be termed as the first step in the business management system process. The needs of the business environment keep on changing, thanks to the rapidly evolving technology. At the same time, the success of an organization is determined by its ability to achieve the 3Rs (doing the right thing, doing it right, and, at the right time) (Northcott & Ma’amora, 2012). This unpredictability makes the BSC one of the most suitable tools to manage the economic challenges faced by organizations. Ordinarily, it is difficult to translate an organization’s strategic statements into specific employee actions. The discrepancy between what the strategy states and/or what can be put into action are a major challenge of the traditional approach to measuring organizational progress. Thus, the BSC makes it possible to convert the strategy into actionable items that can then be assigned to each employee.

Today’s unpredictable business environment means that strategies can change over the cause of time because of economic conditions, as well as leadership changes. This situation raises a question about the importance of strategies as the initial step to building organizational goals. Therefore, it emerges that the scorecard enables the organization to evaluate whether all metrics are being given adequate focus. In other words, a lack of balance indicates that some metrics are receiving more attention relative to others, hence causing instability. For instance, if the emphasis is given only to on-time delivery, aspects such as product quality and employee satisfaction may suffer. Notwithstanding, a natural balance is more useful where the organization achieves a forced balance through the BSC. Being more than a measurement process, the BSC can inspire breakthrough improvements in key areas of the organization, for instance, the product, market development, and customer satisfaction.

The BSC offers managers four different perspectives, which can be utilized to choose measures. Rather than challenging the traditional financial indicators, it complements them (Kaplan & Norton, 1993). The four key areas can be summed up as customers, innovation, internal processes, and improvement activities. This classification of measures is different from the traditional approach in various ways. For instance, the traditional measures used in many organizations are not only bottom-up but also change on a case-by-case basis. On the other hand, the BSC’s measures are fixed in the organization’s strategic objectives. Further, the way to develop a scorecard requires managers to identify only a few critical factors based on the four key perspectives. This situation brings forth a level of focus and ease of implementation that is absent in the traditional measures. Importantly, the BSC utilizes the present and past information to predict future trends. For example, by utilizing information from the four perspectives, the BSC can predict the new types of products that should be developed or ways of improving customer satisfaction.

Presently, many organizations are making efforts to implement processes such as business reengineering, employee empowerment, and total quality management. Therefore, the BSC serves as a focal point for these organizations since it defines priorities. Before these local processes can be implemented in an organization, the management must identify key critical factors that require adjustment. Similarly, the change must be evaluated based on how it will affect the key stakeholders who include managers, employees, investors, and customers. The BSC assists in this process by pointing to the critical success factors and predicting future trends in the organization. Before the adoption of the BSC, many organizations could rely on the one-year budget as the benchmark against all major decisions. Today, the BSC has taken this position, thus becoming the benchmark against which all key developments/projects in an organization are evaluated.

The scorecard is a flexible measurement process that changes depending on the type of organization and areas that need evaluation. As Wu (2012) explains, the BSC cannot be applied uniformly to all businesses since their needs are inherently different. Differences in organizations are caused by operations in different environments, having diverse product strategies, and the prevailing varied levels of competition. Hence, businesses design customized BSCs to suit their mission, strategy, and organizational culture. Indeed, one measure of the BSCs success is its transparency. In other words, a bystander should view the organization’s competitive strategy by simply looking at the scorecard. Below is a discussion of how the BSC operates at Rockwater, a major subsidiary of Brown & Root.

A Sample of BSC at Rockwater

Rockwater is an underwater construction company, which faced fierce competition in the late 1980s. When CEO Norman Chambers was hired in 1989, he understood that the industry had changed tremendously. As such, the company had to reshape its operations. Already, many small companies had left the industry, owing to the sharp competition. Thus, Chambers and his senior management created a new vision to secure the company’s customers from being taken up by competitors (Pietrzak, Paliszkiewicz, & Klepacki, 2015). In the vision, the management decided to focus on safety and quality for its customers. Further, a strategy was designed to achieve this vision. The five elements of Rockwater’s strategy were as follows:

- High degree of customer satisfaction

- Continually improve safety

- Equipment reliability

- Responsiveness

- Cost-effectiveness

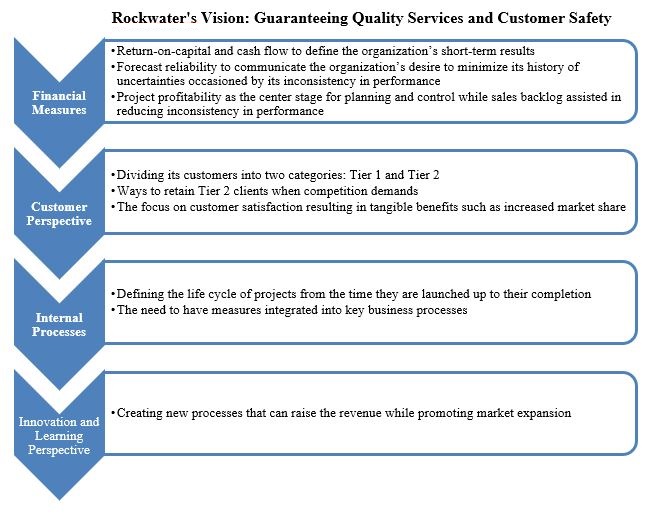

The challenge now regarded how to convert these strategic objectives into actionable targets and goals. Rockwater overcame this challenge by translating the strategic objectives into the BSC’s four performance measures as shown in the Appendix section.

Financial Measures

Under the ‘financial measures’, three metrics were incorporated that would be of importance to the shareholders. First, return-on-capital and cash flow were used to define the organization’s short-term results. On the other hand, forecast reliability communicated the organization’s desire to minimize its history of uncertainties occasioned by its inconsistency in performance. In other words, Rockwater was representing itself as a company that focused on having positive results in all its projects, despite working in a challenging environment (Pietrzak et al., 2015). Additionally, two other financial measures were included, namely, project profitability and sales backlog. Project profitability was used as the center stage for planning and control while sales backlog assisted in reducing inconsistency in performance.

Customer Satisfaction

Under this perspective, the company divided its customers into two categories: Tier 1 and Tier 2. Tier 1 clientele were rich oil companies whose interest was in establishing valuable relationships with contractors while Tier 2 clients were concerned about the prices of the contractors. Hence, a strategy was designed to satisfy both customers. While the focus was clearly on Tier 1 customers, the company needed ways to retain Tier 2 clients when the competition demanded (Pietrzak et al., 2015). In line with the emphasis on quality, the company asked its Tier 1 customers to provide monthly ratings about their satisfaction with Rockwater’s services. In addition, using the BSC, it became apparent that the focus on customer satisfaction was resulting intangible benefits such as increased market share.

Internal Processes

To create healthy measures for the internal processes, Rockwater began defining the life cycle of projects from the time they were launched up to their completion. In other words, the measures extended from when customers’ needs were identified to the time when the demand had been met. These measures were put in place for all the five strategic objectives identified by the organization. Consequently, the focus on internal measures resulted in a change in the way Rockwater’s management used to think and/or operate (Hong & Zhong-Hua, 2013). For example, initially, performance would be assessed at the departmental level. However, the new approach emphasized the need to have measures integrated into key business processes. Particularly, safety became a major priority after it was revealed that the indirect costs of accidents could far outweigh the direct costs.

Innovation and Improvement

Innovativeness is a perspective of the scorecard is intended to facilitate improvement in the other three perspectives, namely, financial, customer, and internal processes. At Rockwater, innovation was geared at creating new processes that would raise revenue while promoting market expansion. Regarding the first objective, revenue increment was measured by evaluating the output of new services while the second objective required a measure of continuous improvement. Overall, the scorecard helped the management of Rockwater to establish a process perspective of its operations. In addition, motivating employees and incorporating customer feedback became easy to effect. Further, other areas that required improvement such as the relationship with suppliers were easily identified and rectified.

Challenges of Implementing the Scorecard

Despite its usefulness in the business environment, the BSC has various problems regarding its implementation. The biggest challenge is not the scorecard itself. Rather, the challenge lies in how the managers view the tool. Many believe that the BSC is a “quick fix” that can be easily implemented to solve all an organization’s problems. However, this view is a misconception that can limit the organization’s potential to attain the full benefits of the scorecard. In reality, the implementation of the scorecard is an evolutionary process that takes time. Hence, to realize the full benefits of the scorecard, an organization must be both patients and committed to the long-term implementation of the process. Failure to commit means that the long-standing benefits will not be achieved. This challenge goes hand in hand with the failure of some organizations to put in place clearly defined metrics. Additionally, these metrics must frequently be evaluated to obtain reliable data. Another challenge with the scorecard is that many organizations lack the appropriate data collection and reporting tools (Hong & Zhong-Hua, 2013). The deficiency causes many of them to focus only on financial data since there are already robust systems for collecting and reporting financial measures. However, the BSC cannot be effective if it focuses only on financial metrics. It means that the other perspectives, namely, customer satisfaction and internal measures, are neglected. In the end, no balance is achieved, a situation, which causes the BSC measurement system to fail in its entirety.

Conclusion

From its invention in the early 1990s, the BSC has evolved from simply being a measurement process to becoming an important strategic management system. By focusing on four key aspects, customer, innovation/improvement, improvement processes, and financial measures, the BSC makes it possible to identify and focus on the critical factors in an organization. Additionally, it serves as a focal point for the implementation of local processes such as quality management and employee empowerment. However, one challenge with the scorecard is that many organizations fail to identify the key metrics. Besides, they are tempted to focus on financial measures only.

References

Bititci, U., Garengo, P., Dörfler, V., & Nudurupati, S. (2012). Performance measurement: Challenges for tomorrow. International Journal of Management Reviews, 14(3), 305-327.

Hong, Y., & Zhong-Hua, Y. (2013). Supply chain dynamic performance measurement based on BSC and SVM. International Journal of Computer Science Issues, 10(1), 271-277.

Kaplan, R. S., & Atkinson, A. A. (2015). Advanced management accounting. New Delhi, India: PHI Learning.

Northcott, D., & Ma’amora, T. (2012). Using the balanced scorecard to manage performance in public sector organizations: Issues and challenges. International Journal of Public Sector Management, 25(3), 166-191.

Norton, D., & Kaplan, R. (1993). Putting the balanced scorecard to work. Harvard Business Review, 71(5), 134-140.

Pietrzak, M., Paliszkiewicz, J., & Klepacki, B. (2015). The application of the balanced scorecard (BSC) in the higher education setting of a Polish university. Online Journal of Applied Knowledge Management, 3(1), 151-164.

Wu, H. (2012). Constructing a strategy map for banking institutions with key performance indicators of the balanced scorecard. Evaluation and Program Planning, 35(3), 303-320.

Appendix

Rockwater’s Sample BSC