Introduction

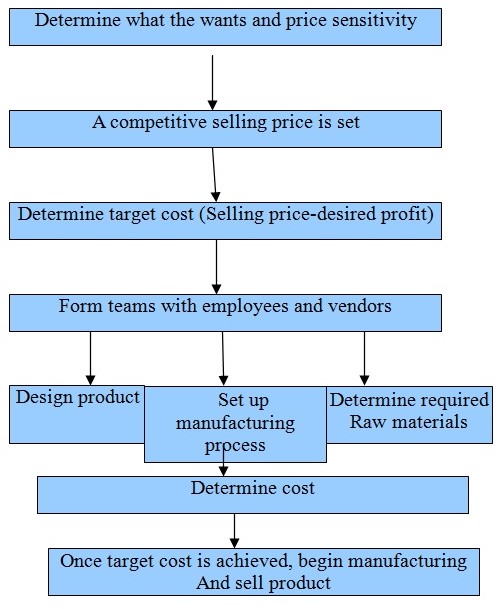

“Target costing is a method used by firms, defined as a cost management tool for reducing the overall cost of a product over its entire life-cycle with the help of production, engineering, research and design” (Clifton, 2005). A lengthier definition is given by Vedder (2008) who explains that “target costing is a disciplined process for determining and achieving a full-stream cost at which a proposed product with specified functionality, performance, and quality must be produced in order to generate the desired profitability at the product’s anticipated selling price over a specified period of time in future”

A target cost is set as a difference between a product’s market price and the desired profit margin. To understand this further, Crosson and Belverd (2011) define a target cost as “the maximum amount of cost that can be incurred on a product and with it, the firm can still earn the required profit margin from that product at a particular selling price”. In the traditional method of setting up prices, the cost of raw material, labor, and overhead costs are summed up and the desired profit is added to determine a product’s selling price.

Target costing is a very common approach to business in Japan. This is especially so in the automobile industry where cost plays a significant role in the sustainability of business (Gharajedaghi, 2011). Automobile companies in Japan have taken this further by decomposing the strategy to each element and part of an automobile. As Yasuhiro and Kazuki (2002) explain, “the designers draft a trial blueprint, and a check is made to see if the estimated cost of the car is within a reasonable distance of the target cost and if not, design changes are made, and a new trial blueprint is drawn up”.

The process is repeated until the manufacturer has attained the most cost-appropriate prototype product. The process also involves continuous evaluation and revision to ensure no gap develops between the target and estimated costs as other market parameters change (Guilding, Karen, and Mike, 2000). The process is similar in other industries where after the process is repeated to a satisfactory level, the final blueprint is handed over to the production department to begin production. Manufactures may not be able to immediately achieve the targeted costs in the first few batches due to the challenges that come with the production of a new model. However, as more batches are produced, consistency is achieved and discrepancies eliminated.

According to Drury (2008), the “target costing approach was developed in recognition of two important characteristics of markets and costs. The first is that many companies have less control over price than they would like to think”. In today’s unpredictable market trends, supply and demand trends are the key determinants of price. Any company that ignores these factors is bound to fail if pricing in profitability. The second characteristic is that the biggest cost of a product is set at the design stage. Once a product is past the design and production stage, there are very few cost-reduction opportunities available. The process of reducing the cost of a product will many times involve re-designing the product, which only adds to the costs of operation.

Target costing

Aims

Understand target costing and the extent to which it allows a company to focus on profit and product in an integrated strategy

Objectives

- Background review of the topic

- Briefly analyze different types of costing and theories supporting them

- Analyze secondary data from different literature review

- Using Wal-mart as a case study, understand how a business can use cost to focus on products and price

Methodology

To cover the objectives of this paper, the methodology used will include the collection and analysis of secondary data and information. It will be collected from the study of books, journals, online articles, magazines, past research projects, and other publications. Books and journals will be used to understand the background of the topic. Online articles and other publications will be used to understand the trends in target costing. This will be done by reviewing the history, development, and future of target costing.

Costing and profitability

Knowing the cost of a product or service makes it possible for businesses to calculate profitability. “Sometimes businesses are not aware that they are making a loss on a specific item or activity because some of the costs that should be attributed to that product or activity have been absorbed elsewhere-so that one part of the business is subsidizing another part” (The Times 100, 2011). The cost of a product is divided into direct and indirect costs. Direct costs are those that are directly associated with the production of a product, while indirect costs are those that cannot be directly tied up to the production of a product but facilitate its completion.

When managing profitability, “the cost-of-production theory of value is the theory that the price of an object or condition is determined by the sum of the cost of resources that went into making it” (Kee, 2010). This theory makes more sense if we assume that there exist several non-produced factors and constant returns to scale in production. When a transaction takes place, it is important to understand that it involves both internal and external costs. It is also important for a business to be able to differentiate between opportunity and accounting costs. Costing theories are further based on an investor’s capability to compare social, private, and external costs in his business (Patty and Michael, 2010).

Steps involved in target costing

As Greve, Christian, and Ulf (2008) explain, “target costing is not a simple activity as it involves many complex steps”.

The steps are broken down into various steps as discussed below;

Specification of investment objective

To ensure maximum benefits from a product using target costing, there need to be clearly set objectives (Weygand, Donald and Paul, 2010). Successful target costing and its management are guided by defined goals and timescale. Each objective has determined importance and a plan as to how it will be achieved. While some investors will take risks and some will do their best to minimize or avoid them, in both instances it is paramount that risks be identified in the earliest stages of the plan. The process of risk identification should also involve identifying constraints that could arise from special situations such as time horizons, increase in the cost of raw materials, liquidity, and legal policies, just to mention a few (Monden, 2000).

Choosing the cost mix

According to Rhodes (2006), “in any investment management, the most important decision is with respect to the cost mix decision”. This step involves the proper proportion of costs involved in making the product. The proportion is determined by several factors such as risk tolerance of the product, current prices of inputs, and period allocated for different goals, among other parameters. It is in this step that a cost management manager has to decide in which class a cost will be placed, as well as which areas of spending will be cut.

Formulation of strategy

Depending with the risks a manager is willing to take, the level of diversification required, and risks involved, the most suitable cost management strategy can be decided on (Maher and Roman, 2005). Formulating a strategy further involves selection of designs after a fundamental and comprehensive analysis of parameters a product developer is interested in focusing on. In manufacturing, a product developer could focus on the shape, durability, ease of the product’s usage, and uniqueness just to mention a few.

Plan execution

This step is one of the most significant determinants of how successful and effective will be. It involves the implementation of formulated strategy, which may include buying or selling bonds at the intended prices. It could also involve the implementation of measures designed to minimize risks or ensure stability in the cash flow.

Strategy revision and evaluation

Just like any other investment management, cost management requires constant revision and evaluation. Changes in the price of inputs automatically change the value of a product in the market (Bragg, 2010). This calls for regular changes on the costing plan to take care of fluctuations. Change of design or a product’s formula may be necessary. Evaluation is done from time to time to determine what is working and what is not. As Ansari, Jan, and Hiroshi (2006) explain, “it helps the investor to realize if the strategy’s returns are in proportion with its risk exposure”.

Factors that influence target costing process

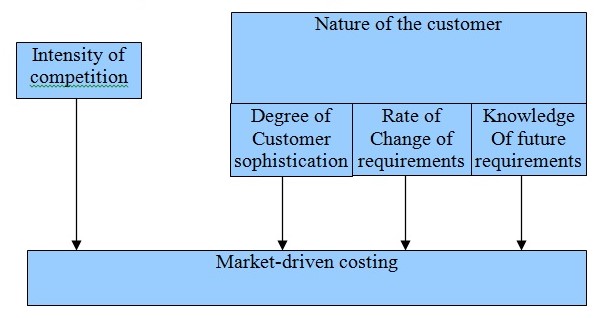

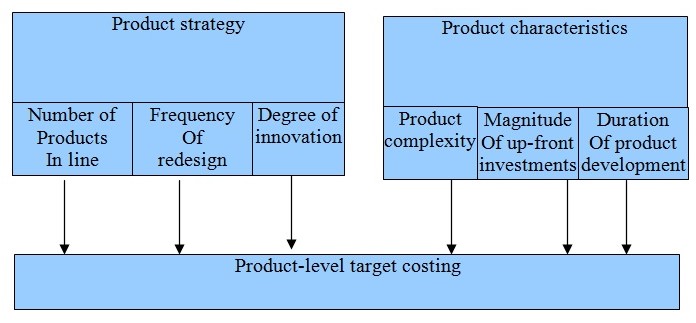

As summarized in Fig. 2 and as explained by Ellram (2000), “all the target costing processes documented contain three major steps, market-driven costing, product-level target costing, and component-level target costing”. The input and desired results may vary depending on the number of factors influencing the process. The cost and complexity of achieving the desired results may further vary with the industry, level of expertise, and different market trends in the industry. A product’s characteristics further play a significant role in determining how the target will be achieved (Bragg and Janice, 2011).

“Each of the steps involved in target costing has defined output: allowable cost, product-level target cost, and component-level target costs respectively” (Nicolini, Cyril, Richard, Alf and Mark, 2000). While these factors are similar in every firm trying to implement target costing, the process is more complex in some industries and may result in different outcomes. The market-driven costing portion is affected by the nature of the target customer, as well as the intensity of the competition in the specific industry. Product-level target costing is influenced by a product’s characteristics, and the firm’s product strategy (Blocher, 2005). Finally, the component-level target costing is affected the company’s supplier-base strategy.

Managing intensity of competition

The amount of attention a company is paying to competitive offerings is highly dependent on the intensity of competition a product is facing (Castellano and Saul, 2003). The levels of importance a company places on its target costing process can be easily judged from the amount of importance it places on competitive offerings. A study conducted on six Japanese companies by Cooper and Regine (1997) “reveals that all the firms had adopted a confrontational strategy because they lacked the ability to develop sustainable competitive advantages over each other”. In markets where competition is stiff, businesses are left with no alternative but to compete with each other on the basis of quality and cost. When this happens, low profit margins, less fast mover advantage and low customer loyalty among other outcomes become a reality to many businesses.

When such a situation occurs, the benefits of target costing cannot be under-estimated. The situation puts businesses in fragile position where they cannot afford to make any mistakes, especially when launching new products. By putting the competitive pressure into consideration when designing new products, a business has higher chances of ensuring that the new product is within is inside its survival zone when it is introduced to the market (Rains, 2011). The results are increased profits for a product, and increased customer loyalty for a product. When the level of competition is low, Ibusuki and Paulo (2007) explain that strategies which are less confrontational strategies can be used.

In an industry where competitors easily bring out the ‘me-too’ products, it may be difficult for a company to maintain competitive advantage over its competitors on the basis of other parameters such as quality. The recent world global crisis left many economies and consumers struggling, making price one of the most significant factors in the markets. As a result, an advantage over competitors in the market puts a company in a very advantageous position.

Nature of the customer

The intensity of customer analysis carried out by businesses in influenced by customer’s characteristics. The most of these characteristics as identified by Ellram (2002) are; degree of sophistication, degree to which they understand their future requirements, and rate at which their expectations and needs are changing. As Swenson (2003) explains “these three characteristics appear to help determine the benefits that a firm can potentially derive from target costing because they deal with the width, rate of change of location, and ease of predicting the location of survival zones”. Target costing is particularly beneficial to businesses whose competing environments have smaller survival zones. Locations with such zones are changing rapidly, and businesses need to stay constantly updated on the changes (Lal and Seema, 2009).

Understanding customer satisfaction enables a business know how sensitive its customers are to differences in functionality, price and quality among other parameters of products in the market (Lockamy and Wilbur, 2000). The more sophisticated a customer is, the more they are likely to detect the smallest on differences in competitive products. Target costing requires a deep understanding of target customers through constant interaction, surveys and feedback (Crosson and Belverd, 2011). In the process of doing so, a business is able to satisfy its customers by having products custom made to meet their needs.

“The rate at which customer requirements change defines how rapidly the location of survival zones move over time” (Ewert and Christian, 1999). The process of understanding the requirements over a long period of period allows a business to develop a pattern that can be used to predict customers’ future needs. Target costing is therefore a practice that can be used to develop products that keep a business ahead of others. It is also easy for a business to schedule changes early and avoid producing products that may be considered already irrelevant in the market.

In environments where consumer preferences are changing rapidly, target costing is more beneficial. Using target costing it is easier for a business to launch products that are within the survival zone in the market. When consumer expectations and requirements are stable, businesses have a tendency to relax on innovations (Smith, 2007). However, the opposite happens, they are forced to expend significant amounts of resources and effort to understand and predict customers’ needs. It is such situations that have led to constant innovations in the market, and more profitability for the most creative companies. The best example of how profitable research and new developments can be is the communication devices industry. New products each day attracts customers who are willing to stay updated on new solutions in the market. As a result, companies are able to launch and sell a new product every often, a trend that has translated to an exponential growth of the industry. Companies who are able to keep up with the new developments in the market have remained profitable, even during the recent global economic crisis. This proves how important understanding customers’ needs can be to a business. Target costing supports this through a need to predict the needs in order to achieve the best cost for the products before they are needed and released to the market ((Ellram, 2006).

The degree to which customers understand their future product requirement

The more customers understand their needs, the easier to become for a business to rely on their preferences and feedback (Hibbets, Tom and Wilfried, 2003). Survey of what they expect can be trusted and results used to locate future survival zones. In contrast, when customers are not certain of their needs and preferences in future, businesses have to spend a lot of money and resources to locate future survival zones. Many times this is hard and they are forced to launch products that eventually fail due to poor approximation of survival zones.

Customers have a varying understanding of their future needs for different industries. For example, customers are more aware of what they want in future for food products, but thus may not be so in the electronic industry. As a result, when using customers’ feedback on what they need in future, a business must put this factor into consideration. A business would be in a safer zone if they can exceed their expectations. When this happens, target costing becomes easier since business saves money by being ahead of what customers expect.

Using target costing to manage profits and products

Proactive approach to cost management

Target costing allows businesses to take a proactive approach to cost management. Traditionally, businesses manage costs when a product is already finished. Direct costs which make up more than half the cost of a product remain a challenge to many investors. Target costing as has been evident in many Japanese businesses can help a business manage costs by cutting on it at the design level. By having a set cost of production, a business is able to have control of their profitability. A proactive approach reduces speculation and yet makes it possible to approximate profits.

Orients businesses towards customers

Businesses can use targeting costing to orient themselves towards business. This way, a business knows what to expect from the customers, as well as what is expected of them. Since target costing is very much dependent on survival zones, a business is forced to understand comprehensively. This includes their needs, expectations and spending trends, among others. It further forces a business to understand its competitors, strengths and weaknesses. This kind of knowledge and market understanding empowers a business to design and product goods that are needed in the market. Chances of being in the low survival zones are reduced and profitability soars.

Breaks down barriers between departments

For a business to succeed in cost management, costs have to be cut in all departments. The design and production of a product is very dependent on the logistics, purchasing, human resource, production and quality department. These departments are responsible for the cost of raw materials, how they are managed, designed and how the final product looks like as well as how much it costs. Working together in the initial stages of a product keeps the department and their activities synchronized. When products are out in the market, managing them is an easier task since every department is well conversant with its strengths and weaknesses.

Implementation enhances employee awareness and empowerment

Target costing is very dependent of the customers’ ability to understand and interpret their future needs. It is through feedback and trusting customers to make decisions on what they will need in future that a business is able to begin design. When employees are put in a situation where they have to work with guidance from customers, it enables them to go out of their way to understand what they are involved in. This ensures that employees understand not only the business and its products, but also the customers and their needs. Furthermore, target costing involves a lot of training on issues related to cost.

For a business to fully realize target costing, employees need to understand their role in the process. For example, the production team needs to learn about cost cutting through different techniques such as total production management (TPM), quality assurance, total quality management (TQM), as well as other production pillars. The process of achieving this in a business involves constant training and more productive employees. Increased output further improves profitability in a business.

Foster partnerships with suppliers

As Seuring (2002) explains, suppliers play a significant role in a business’ ability to work with minimum input costs. This is evident through the retail industry who are no longer dependent on wholesalers in a bid to have reduced costs. By sourcing materials directly from a manufacturer, they are able to enjoy reduced cost advantages. For a business to cut its cost of a product, it needs to have suppliers who value consistent and can offer the best prices. Through negotiations, a business can achieve this and further strengthen its relationship with suppliers. Through such developments, a business is able to develop and maintain good quality, as well as improve profitability.

Minimize non value-added activities

It is through target costing that a business is able to identify areas where costs can be reduced. Non-value added activities account for a big percentage of indirect costs and yet can be reduced by developing a cost-conscious tradition in a company. Through business techniques such as TPM, employees conduct regular audit procedures to indentify where loses are occurring. This has been achieved in Japan through kaizens and office designs that minimize time wastage. Total production management encourages selection of lowest cost value added activities in both the goods and services sectors.

Reduced time to market

A business is able to grow its profitability through target costing by reducing the time required to market a product. This is especially true in industries where customers are extremely price conscious. Through target costing, a business is able to maintain stable pricing of its products in the markets. This helps them grow customer loyalty. Target costing helps a business introduce products to a market with a full awareness of the costs future pricing trends of a market. It is therefore possible to maintain the same prices in fluctuating markets, which puts a product in an advantageous position compared to its competitors.

Design

As Helms, Lawrence, Joe and Mathew (2005) explain, “the difference between target costing and other approaches to product development is profound. Instead of designing the product and then finding out how much it costs, the target cost is set first and then the product is designed to that the target cost is attained”. To achieve intended results in target costing, cost reduction through design is paramount. Businesses are able to use design to offer best prices in the market by use inexpensive parts, designing products that are simple to make, making products that are robust and reliable, and designing target driven products. This way, a business is able to give reasonable prices to customers, as well ensure their needs for quality are met.

Furthermore, a business is able to earn customers’ trust through products that are easy to use and sensitive to economic factors affecting different regions. As Afonso, Manuel, Antonio and Ana (2008) argue, “target costing is relentless in pushing the organization to establish and achieve the cost targets. It brings the factory floor together with the supporting departments to ensure there is a total understanding of the market for a product”. The strategy has received a lot of support from businesses, especially in the manufacturing sector for its capability to drive blunt market realities to the business. Through such drives and measures, business benefit by growing their profitability and developing products that can effectively compete in the market.

Executing target costing

Execution is the most significant stage of target costing. The key to successful execution is to keep counter-checking the plan versus the actual process constantly. It is also important to have different levels of management of the process. Corrective measures should be addressed in well-spaced reviews and without any delays. The key tools for execution include;

Sufficient chart (SC)

As Ansari (1997) explains, “the sufficient chart is the highest level of monitoring for target costing”. It is used to track actual costs, profit margins and projected costs. Where applicable, it is also used to track target profit and projected prices in the market. The projected costs are based on element tracking lists, one of the execution tools (Dekker and Peter, 2003). Sufficient chart is considered a key evaluation and monitoring tool for the product line. It is further used to measure performance as far as target margins are considered.

Key task monitor (KTM)

Key task monitor is significant for every project trying to implement price targeting. It is considered as the implementation schedule for target costing. Important parameters to consider in KTM include individual tasks, labor, the investor and scheduled dates for each of the tasks.

Element Tracking list (ETL)

According to Cooper and Regine (1998), element tracking list is “the master list of each cost reduction project that the team is working on for the product line”. It tracks customer requirements, dates, project owners, product description, key tasks and level of implementations, among other key parameters of a project.

Target costing in Wal-mart

Wal-mart is an American multinational corporation running over 8,500 stores. The company trades in over 15 different countries under different names and is ranked 18th in the list of world’s largest public corporations. The store operates through three primary channels: Wal-Mart Stores, Sam’s Club, and International. Its stores channels include reduction stores, ‘super centers’, and neighborhood markets in the US, as well as walmart.com.

Due to the stiff competition in the retail industry, the business has had to adopt measures that put it ahead of the rest. “Since cost is the most important tool that drives businesses to success, the strategy for managing cost is also important for business to succeed especially for giant retailer like Wal-mart” (n.a., 2011). While target costing is largely discussed in reference to the manufacturing industry, the retail industry can use it to cut and stabilize costs in their businesses. Just like in every other sector, a retail business has direct and indirect costs. Fixed costs do not change and are not influenced by the business’ sales volumes.

Target costing in Wal-mart is mainly through a strong bargaining power with suppliers. The business holds so much of the market share and offers a lot of business to manufactures, making it a valuable asset to its suppliers. This gives the company a lot of power because any threat to lose business in the company creates a scare among suppliers. This is especially in the industries where substitute products are easily available. In addition, the company deals with large suppliers such as Coca Cola, who can offer the company large amounts of discounts. Through such mechanisms, Wal-Mart is able to access its products in the lowest prices possible. By having the minimum cost of a product, they are then able to manipulate the other costs to achieve their target cost.

Target costing in Wal-mart is also implemented through managing the cost of accessing and distributing the products. The company’s cost management approaches include budgeting payroll, eliminating irrelevant costs, saving on the cost of keeping the products, and taking advantage of technology to minimize labor requirements. One way through which Wal-mart implements target costing is managing payroll. The amounts of money spend on distributing a certain volume of goods can be reduced if the business is able to trace its payroll cost. The company does this by reviewing the cost per department and frequently comparing the costs to the costs on the target plan.

Wal-mart also implements target costing through an elimination approach. The business does this by eliminating all unnecessary costs. As defined by Weygand, Donald and Paul (2010) “unnecessary cost is unnoticeable cost that already occurred but customers are not willing to pay for it such as box in/out cost, moving cost or recycling cost”.

Conclusion

Target costing is a very common approach to business in Japan. This is especially so in the automobile industry where cost plays a significant role in sustainability of business (Gharajedaghi, 2011). Automobile companies in Japan have taken this further by decomposing the strategy to each element and part of an automobile. Costing theories are further based on an investor’s capability to compare social, private and external costs in his business (Patty and Michael, 2010). In manufacturing, the need to have manufacturing and non-manufacturing costs is critical. When such factors are understood by an investor, then the relationship between costs and profitability begin to make sense.

The benefits of target costing in managing products and profits are many. Target costing allows businesses to take a proactive approach to cost management. A proactive approach reduces speculation and yet makes it possible to approximate profits. Businesses can use targeting costing to orient themselves towards business. Since target costing is very much dependent on survival zones, a business is forced to understand comprehensively. It is also notable from the research that the design and production of a product is very dependent on the logistics, purchasing, human resource, production and quality department. This means that target costing supports a business’ understanding of these issues.

Target costing is very dependent of the customers’ ability to understand and interpret their future needs. It is through feedback and trusting customers to make decisions on what they will need in future that a business is able to begin design. It further allows this to happen through a good management of suppliers. This is evident through the retail industry that is no longer dependent on wholesalers in a bid to have reduced costs. By sourcing materials directly from a manufacturer, they are able to enjoy reduced cost advantages. For a business to cut its cost of a product, it needs to have suppliers who value consistent and can offer the best prices.

Recommendations

For businesses to fully benefit from target costing, some business tools and techniques have to be in place. It is important that through business techniques such as TPM, employees conduct regular audit procedures to indentify where loses are occurring. This has been achieved in Japan through business solutions and office designs that minimize time wastage and reduce cost. Production management techniques implemented in a business must encourage the selection of lowest cost value added activities. It is also important the businesses be realistic enough when setting target costs to reduce the number of times they need to create a new plan.

The process of target costing must include sufficient research to ensure that the relevant team makes informed decisions. The first step should be a comprehensive market research to ensure that decisions are made based on facts. Products characteristics must meet customers’ needs. The planned selling price must be competitive enough and take into consideration what the product is offering to the market. It is also important that the design, engineering, and supply department work together to ensure consistency in the process.

Reflective report

In this module, I have studied various principles of costing. Understanding the theories behind costing, factors that influence it and costing trends in present times has given me valuable insights about business management. It has further helped me understand the value of constantly putting customers into consideration when one is doing business. This report has covered different aspects of target costing. The process of gathering information has helped me understand the concept of target costing, its significance in different industries, and the differences between it and other costing strategies. The paper was focused on how it is used in businesses to manage costs and products, which further helped me understand profitability and product management in businesses.

I completed this paper through a step-by-step analysis of each of the topics that needed to be covered. The first step involved understanding the assignment and what was required of me. This enabled me to set the aim and objectives of the paper. The second step involved collecting material and information on the related topic. In an age where information is easily available online, too much information can be overwhelming, hence the need to sort out material before commencing on a task. This exercise taught me how time consuming information management can be, and the need to allocate sufficient time to the task. The last step, which was writing and compiling the paper then followed.

The methodology, which was done through collection and analysis of secondary data and information, has helped me improve my data and information skills. By using books, journals, online articles, magazines, past research projects and other publications to develop an argument for this paper, I have further improved my research development skills. I have also learnt how to use different resources for different purposes such as using books and journals to understand the background of the topic and using online articles and other publications will be used to understand the trends in target costing as done in this paper.

The process of gathering information has not only been a good experience, but also very informative. In the process of accumulating information, I have learnt many other cost-related issues, which may not be significant for this particular research paper.

Completion of this paper further involved analysis and integration of information from different sources. The process of compiling it to come up with a comprehensive paper has helped me improve my writing, interpreting and analytical skills. Through the process, I have learned how to apply the concepts taught to me in this module in practical situations and in scenarios requiring critical analysis and thinking. It has also been possible for me to test my capabilities in different areas of research writing.

Interaction with different authors through their work was a great experience for me. Through their work on different topics, which I had to understand to complete my paper, I learnt how to compile ideas to complete an academic paper or book. The books and scholarly journals were particularly informative and enabled me get a broader perspective of the difference between business practices in different companies and even countries. Since this was an accounting paper, I was able to gather relevant information that will be beneficial as I complete my other tasks and modules. I realized that accounting is a broad topic and it adequately addresses different concerns that an average consumer would be interested in.

As far as my skills are concerned, the greatest areas of weakness included not doing background research on time to allow me a humble time when writing the final paper. Doing the two tasks at the same time can be overwhelming and may cause confusion of ideas. However, this has taught me the importance of planning for a task before commencing. I was able to overcome the challenge by developing a schedule based on the time available. This way, I was able to set a time limit for every topic and ensure that I was as disciplined as possible.

In order to improve on my research writing skills and identified weaknesses, I plan to write research papers on the different modules we are covering in school, and have them reviewed by relevant teachers. This will be done after consultation with my teachers to ensure they approve the topics I choose, as well as help me develop relevant guidelines for each project. The research projects will then be submitted to the same teachers for review and corrections where appropriate. This will be done with the aim of improving my confidence levels in preparation to my final research project and similar tasks in future.

Time management is a critical element in my self-improvement plan. As learn from this particular research, background research is important for writing a good research paper and should be done before I start the writing task. Due to my other commitments, I plan to write a timetable and give the number of papers I should write as submit by a given time. I will set objectives and goals and review them often to ensure I accomplish them by the set timescale. As I do this, I am confident that the exercise will help me polish my writing, time management and critical analysis in future. I have already started preparing for the plan by collecting various research projects by different authors in the past to help me understand the required resources and work on making sure that they are in place before I start. My next plan will be to speak with my tutor to help me compile a list of research topics that I can write on.

Overall, I have enjoyed the process of writing this task and know that it is a step towards perfecting my research writing skills. I have enjoyed learning about business aspects that affect me even as a consumer. I have also enjoyed the feeling that comes with accomplishing a task and doing so on time. The task has left me with improved confidence levels in knowing that I am capable of gathering and compiling information to complete a research task.

Reference List

Afonso, P. Manuel, N., Antonio, P. and Ana, B., 2008. The influence of time-to-market and target costing in the new product development success. International Journal of Production Economics, 115(2): 559-568.

Ansari, S., 1997. Target costing: The next frontier in strategic cost management: The CAM-I target cost-core group. Chicago: Irwin Professional Publications.

Ansari, S., Jan, B., and Hiroshi, O., 2006. Target costing: Unchattered research territory. Handbooks of Management Accounting Research, 2: pp.507-530.

Bragg,S., 2010. Business ratios and formulas: A comprehensive guide. Hoboken, N.J.: Wiley.

Bragg, S.M. and Janice, M.R., 2011. The controller’s function: The work of the managerial accountant. Hoboken, N.J.: Wiley.

Blocher, E., 2005. Cost management: A strategic emphasis. Boston: McGraw-Hill.

Castellano, J.F and Saul, J., 2003. Speed splasher: An interactive, team based target costing exercise. Journal of Accounting Education, 2(2): 149-155.

Clifton, M.B., 2005. Target costing: Market driven product design. New York: Taylor & Francis.

Cooper, R. and Regine, S., 1998. Target costing and value engineering. Portland, Or.: Productivity Press.

Cooper, R. and Slagmulder, R., 1997. Factors influencing the target costing process: Lessons from Japanese practice. The Claremont Graduate School.

Cooper, R. and Slagmulder, R., 1998. Target costing and value engineering. Portland, Or.: Productivity Press.

Crosson, S.V. and Belverd, E.V., 2011. Managerial accounting. Mason, OH: South-Western Cengage Learning.

Dekker, H. and Peter, S., 2003. A survey of the adoption and use of target costing in dutch firms. International Journal of Production Economics, 3(11), pp. 293-305.

Drury, C., 2008. Management and cost accounting. London: Cengage Learning EMEA.

Ellram, L.M., 2000. Purchasing and supply management’s participation in the target costing process. Journal of Supply Chain Management, 36(2): 39-51.

Ellram, L.M., 2002. Supply management’s involvement in the target costing process. European Journal of Purchasing & Supply Management, 8(4), 235-244.

Ellram, L.M., 2006. The implementation of target costing in the United States: Theory Vs. Practice. Journal of Supply Chain Management, 42(1): 13-26.

Ewert, R. and Christian, E., 1999. Target costing, co-ordination and strategic cost management. European Accounting Review, 8(1): 13-67.

Gharajedaghi, J., 2011. Systems thinking: Managing chaos and complexity: A platform for designing business architecture. Burlington, MA: Morgan Kaufmann.

Greve, J., Christian,A., and Ulf, N., 2008. The impact of competition and uncertainity on the adoption of target costing. International Journal of Production Economics, 115(1): 92-103.

Guilding, C., Karen, S.C. and Mike, T., 2000. An international comparison of strategic management accounting practices. Management Accounting Research, 11(1): 113-135.

Helms, M.M., Lawrence, P.E., Joe, T.B. and Mathew, W.G., 2005. Managerial implications of target costing. Competitiveness Review: An International Business Journal Incorporating Journal Competitiveness, 15(1): 49-56.

Hibbets, A.R., Tom, A. and Wilfried, F., 2003. The competitive environment and strategy of targeting costing implementers: Evidence from the field. Journal of Managerial Issues, 15(1): 65-81.

Ibusuki, U. and Paulo, C. K., 2007. Product development process with focus on value engineering and target-costing: A case study in an automotive company. International Journal of Production Economics, 105(2): 459-474.

Kee, R., 2010. The efficiency of target costing for evaluating product related decisions. International Journal of Production Economics, 126(2), pp.204-211.

Lal, J. and Seema, S., 2009. Cost accounting. New Delhi: Tata McGraw-Hill.

Lockamy, A. and Wilbur, I.S., 2000. Target costing for supply chain management: Criteria and selection. Industrial Management & Data Systems, 100(5): 201-218.

Maher, M.W. and Roman, L.W., 2005. Handbook of cost management. Hoboken, N.J.: Wiley.

Monden, Y., 2000. Japanese cost management. London: Imperial College Press. n.a., 2011. Strategy for managing cost. Web.

Nicolini, D., Cyril, T., Richard, T, Alf, O., and Mark, S., 2000. Can target costing and whole life costing be applied in the construction industry? Evidence from two case studies. British Journal of Management, 11(4): 303-324.

Patty, R.M. and Michael, A.D., 2010. The end of project overruns: Lean and beyond for engineering, procurement, and construction. Boca Raton: Universal Publishers.

Rains, J., 2011. Target cost management: The ladder to global survival and success. Boca Raton: CRC Press.

Rhodes, E., 2006. Supply chains and total product systems. Malden, Mass: Blackwell.

Seuring, S., 2002. Cost management in supply chains. Heidelberg Physica-Verl.

Smith, J.A., 2007. Handbook of management accounting. Amsterdam: Cima Pub.

Swenson, D., 2003. Target costing best practices. Management Accounting Quarterly, 4(2): 12-17.

The Times 100, 2011. Costing and profitability. Web.

Vedder, H., 2008. The target costing approach an explanation of the goals and method. Munchen GRIN Verlag.

Weygand, J.J., Donald, E.K. and Paul, D.K., 2010. Managerial accounting: Tools for business decision making. Hoboken, NJ: Wiley.

Yasuhiro, M. and Kazuki, H., 2002. Target costing-Kaizen costing in Japanese automobile companies. Journal of Management Accounting Research, 3, pp. 16-34.

Appendices